Since the COVID pandemic and the uprising of social justice causes, especially after the events of George Floyd in 2020, I have been reflecting on this strange shift in society and trying to understand this change on a deeper level. From COVID and all of the messages from companies to ‘do the right thing’ with masks, distancing, or even staying home — which I thought was an absurd strategy, considering a capitalist running a business would want as much of your labor for their product even if it is a pandemic market — something seemed off. This was an early sign, and it was after the unrest resulting from the murder of George Floyd that you started to see these social justice slogans relating to the solidarity behind black and brown bodies in company releases, or the changing of company logos to rainbow flags during pride month, or the use of the buzzword sustainability which I discuss in a publication here.

For the record there is nothing wrong with advocating for social justice, some of it I feel is warranted, some I feel is grifting for attention, and others are just downright cynical and dangerous. For example, my experience with indigenous pedagogy and indigenous ways of knowing provide me the opportunity to challenge companies who would like to take the historical strife relating to Aboriginal Peoples in a glorification direction, rather than a respectful and rational direction which is more accepted by Aboriginal tribes — after all, reconciliation is about coming together rather than exploitation.

However, this ‘off-ness’ with cohesion of business and social activism never been seen before really was a 180-degree shift for some companies, almost ironical. I mean we have McDonalds turning its golden arches upside down for International Women’s Day in solidarity for gender equity. Even though it is shown that the food at McDonalds, over a period of time, can cause heart disease which takes the lives of nearly 300,000 women a year according to the CDC. Or how Raytheon Technologies – who specialize in weapons manufacturing – decided to change their logo to reflect all of the colours for the LGBTQIA+ and BIPOC marginalized contingency. Even though their bombs routinely killed marginalized Afghanis and Iraqis over the past 20 years.

It felt like a script out of a South Park episode. The hypocrisy was astounding, and it was when I purchased Woke Inc. by Vivek Ramaswamy that this became all so clear.

ESG: Origins and Outcomes

It was Chapter 5 of Vivek’s book titled: The ESG Bubble, is where I was introduced to the concept of Environmental Social Governance (ESG). Vivek starts the chapter being called to testify about new Security and Exchange Commission (SEC) rules being implemented so companies are to disclose their ESG markers with transparency. Vivek himself points out that ESG is a massive bubble due to investing error, contradictions, and the amount of cash flow propping up investment based on financial fads. This was a good introduction, but I wanted to go deeper into the origins of ESG and to ingratiate myself with the narrative around it.

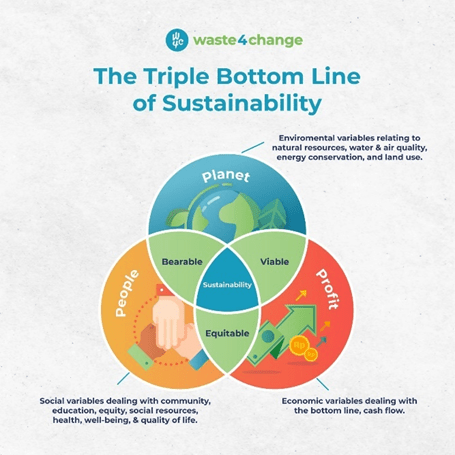

The origins of ESG itself are vague, but it can be traced back to John Elkington, Bob Eccles, and the United Nations (UN). In 1992, the UN held a conference on the environment and future development in Rio De Janeiro. This was commonly referred to as The Rio Summit and it set the ground rules for today’s social and environmental ideas through sustainable development goals. This of course laid the groundwork as many world leaders and special dignitaries attended this summit and was impactful for the socio-political rhetoric heading into the new millennium. This led to author John Elkington in 1994 to coin the phrase ‘triple bottom line’ denoting a sustainability framework that examines a company’s social, environmental, and economic impact. The goal is to reach a harmonious balance of sustainability through coordinating business practices focusing on people, profit, and planet.

Bob Eccles – well known Harvard Business School professor – is considered the leading authority on ESG in the modern millennia. Through implementation and investment strategy surrounding ESG paired with access to the highest echelons of academic institutions; Eccles was a key influencer in the 2006 UN Principles for Responsible Investment (UNPRI) and numerous ESG analytic firms like such as MSCI, FTSE Russell, and Sustainalytics which act as the referees to the modern ESG game. One key theme that I notice is the web of different entities involved with the highest echelons of business, academia, and government institutions. Considering the S in this stands for social, a large deal of individuals (ones who are not CEO’s, university administrators, and world leaders) have no say in the process of ESG investment creation.

First thing to point out, what is ESG to the layperson? Well, it is essentially an investment metric based on environmental and social causes in the world. Simpler, companies can earn money by being environmentally and socially conscious to certain causes. The higher a company’s ESG score, the more access to ESG investment they can obtain to accrue more shareholder profit. Raytheon supporting pride and McDonald’s with International Women’s Day are all examples of bolstering their ESG profile to take a slice of the almost 40 trillion ESG assets pie. Vivek correctly notes the contradictions of an ‘apparent socially just company’ is not to maximize profits through environmental social governance; rather, a true environmental social governance company should place profit behind…well…social governance which is not the case here. I would also add that it is clear a profit motive is involved, after all, McDonalds does not sell burgers because they feel the world is a better place with their burgers. They are relatively cheap to make, they earn roughly a 400% markup on hamburgers, and they use their food to levy investments in the big money maker: real estate, making McDonalds one of the largest real estate holding companies in the world.

What I noticed with ESG is the large, multi-faceted, and connected web of different powers coalescing around this. From key hedge fund and investment firms in the private sector, to multi-government organizations and NGO’s like the UN and the WEF, to academic institutions like Harvard all create an effective stable of groups expanding this investment ideology impacting socio-economic governance for the ‘common good’. ESG is marketing in a way, it is marketing this idea of social and environmental support, only to earn money off allegiance. Another way to view ESG is as a marketing scheme given its offerings are based of a vague sense of understanding of what ESG entails. For example, what is considered ESG and what is considered non-ESG? According to the Wall Street Journal, ESG investments take 3 approaches to how they prospect, or rank companies based on ESG metrics:

- Exclusionary

- Single Theme

- Best in Class

Exclusionary companies are companies who are considered socially difficult or undesirable to investors given their social proclivities (e.g. pornography, weapons manufacturers, alcohol, tobacco, gaming etc.). Single theme describes companies’ willingness to focus on one – predominantly progressive theme relating to social justice such as gender equity, racial justice, or environmental sustainability. Best in class investing uses a loose definition of competition based on the investment goals. In the case for ESG, an example would be Oil Company A built a windfarm and hired 4 female executives compared to Oil Company B through F who pointed out it is Pride Month for LGBTQ individuals, and each hired 1 female executive. All have engaged with ESG in some form, but Company A would have more access to ESG investments as they were the best in class by doing more ESG than Companies B through F.

If you have not already noticed, there is a host of contradictory and hypocritical actions within these 3 approaches to investing. First off, what makes a company like Anheuser-Busch less virtuous than a company like Amazon, leading to exclusion? After all, one can purchase groceries on Amazon, including wine and beer which takes out the exclusionary principle. In addition, I have not heard reports of poor working conditions and treatment of workers in the AB manufacturing plants, unlike Amazon. Second, we have already showcased the absurd transparency between companies like McDonalds and Raytheon. Third, the ignorance that one company wins the ‘woke olympics’ over another company, all while ignoring they are oil companies, or alcoholic producers, or technocratic giants who have had histories with environmental degradation and labor challenges (just look back from early to late 20th century).

The Psychology of ESG

One area of analysis that seems to be missed is the psychology surrounding why ESG investments are popular and why companies are doing it. The cynical anti-capitalist would say that it is purely for money and gaining more power to oppress the masses. Sure, that may be a thread, but it is myopic considering we still have choice not to use companies like Amazon, McDonalds, or Raytheon. You as a fighter for the cause can go to independent stores and shop for good forgoing the convenience of Amazon, you can go to local delis or grocers and not be convened by McDonalds, you can support and actively vote for individuals who would like to cut the military budget (Rand Paul) which would challenge the business model of Raytheon. Companies know that as well, but they still engage – why? Because they also know humans quite well, and they know your fighting is a bluff and that you love the convenience of Amazon shopping, McDonald’s food, and the drama that geopolitical events through manufactured consent.

They know it, and you cannot stop it, psychologically speaking. These companies know it so much, they fall victim to their own shadow projection, commonly attributed to psychologist Carl Jung. Jungian shadow projection comes from his 1951 work, Phenomenology of the Self, describing how an individual’s unconscious instinct sees in others what they might not see in themselves creating an inferiority complex and casting that shadow outward to avoid confronting their own shortcomings. An example is the narcissist railing and hollering at someone for their own self-centeredness unable to self-actualize their own self-centeredness.

ESG works in the same way. Certain companies, like the ones we mentioned, cannot come to terms with their own dark actions as companies; thus, need to project the failure of everyone else’s piety to reflect their own failure. A clear example of this relates to a bevy of companies following the so-called ‘progressive line’ on human rights all while exploiting labor out of Uighur Muslims held in concentration camps in communist China. Companies also included are large multi-national tech companies, the robber barons of our day.

When confronted, usually there is no comment, a guide to the company’s legal team, or an obfuscated shadow projection that attempts to take their negative and twist it into some sort of weird positive that they are ‘striving for change’, and that is the grift is of ESG, this trillion-dollar house of cards all built on the flimsy strive for change. This flimsy base relates to Vivek’s knowledge around the ESG market being propped up through money with no clear return on investment attached. To say ESG bonds are doomed is an understatement considering the hubris of corporations and how governments are generally terrible corporate stewards will lead to the ESG bubble burst and a massive loss similar to the 2008 financial crisis.

Doomed Investing

In addition to Vivek’s comparison to the 2008 financial crisis dooming ESG investment, I see another similarity to another corporate fraud scheme relating to the Enron scandal from 2000-2003. One of the biggest downfalls relating to Enron had to do with their ‘mark to market’ strategy which simply means adding unrealized future gains onto current income statements. So, if you have a factory that was set to make 1 Million in 2002, and you see its potential future earnings being 10 Million in 2012 based on forecasting, you add the 10 Million into your books for 2002. The reason for this is even if that factory is only making 1 Million per year and your actual accounting reflect in 2003 your earnings being 2 Million, you make it look like10 Million which looks good on paper and for investments. That was the key issue, investments. Investors in Enron thought this was a massively successful company based on earnings, even though actual earnings were 5 to 10% of the inflated numbers.

Mark to market strategies is similar with ESG investing, as investment firms themselves are banking on future earnings with this 40 – soon to be 50 trillion asset market by 2025. Key questions to ask – in relation to the mark to market strategy: where is the money coming from? And how is the money getting there? So, if we have money from Exxon, McDonalds, and other multi-national corporations creating this bubble of ESG investments, and these – much like all companies – must cut their growth mindset to be ESG compliant, that means a massive drop in the 50 trillion investment calculation meaning less money — unless there is a floatation propping up the investment such as the IMF or World Bank? If so, then the mark to market will be less that unrealized gains are added willy-nilly; rather, printing and inflation being the source. Sure, the money is there but the inflation reduces the value of money, the more money that is printed the more it reverts to its original form of cheap pulp. It introduces dilemma for ESG companies as well, do we actually commit to our goals of environmental and sustainable targets and lose money? Or do we continue to earn profits and lose the investment with ESG? Much like how governments are bad at business, businesses are bad at philosophical dilemmas.

ESG investments are also generally weak investments, much like Enron and their infrastructure failure in India due to government and lack of cultural foresight, companies attempt to make good investments where no good investments could be found. Let’s take automobiles as an example. A car is generally one of the worst investments considering dealerships bank on new-car purchases, while most cars on the road are leased or used which forces demand for used cars high and prices low. But the investment in the electric car has skyrocketed and is a key aspect in ESG investments especially manufacturing. Here is the main question: say we have switched to 100% electric vehicle, what next? Well, the market will be saturated with new and used electric cars, with leasing needed to be an option for buyers to get into the dealership. So yes, you fixed the environmental problem, but you have not fixed the financial problem with weak investments considering we will be in the same spot leased and used electric cars will dominate the road, and new electric cars will sit on the lot as the toxic battery compounds degrade into the environment.

Continuing with weak investments, the term ‘greenwashing’ has entered the lexicon of ESG as companies strive to achieve environmental markers, while their environmental policies may be hurting in other environmental and even social areas. We can use wind power as an example. Many companies would like to invest in wind power because it is a physical representation of green energy production for marketing.

However, in reality, wind technology is not that self sufficient and not that stable according to many expert accounts. Craig Rucker – President of the non-profit Committee for a Constructive Tomorrow environmental group – suggests in his article: Wind Power: Our Least Sustainable Resource, that wind power is not only environmentally unstable – but socially and economically unstable. Environmental instability is obvious as Rucker points out the amount of steel and land degradation wind turbines cause – which is corroborated by peer-reviewed evidence. One study suggests the environmental issues from disposal of turbine blades in landfills causes negative externalities on wildlife through methane release or hazardous off-gases. Another study predicting that there will be 43 million tonnes of blade waste by 2050, close to half contributed by China, and causing even more harmful emissions for continued production and disposal. As for social and economic instability, Rucker assesses the cost of these projects causes a burden on taxpayers due to the cost of transmission lines, not to mention that wind nets a negative 2-3 traditional job in replacement of wind. In addition, job losses create social instability leading to impacts on planetary and personal health.

Essentially, you can boil down the case of Enron – and ESG to an extent – as a house of cards propped up on a tightrope over shark infested waters. From its mark to market strategy of falsely inflating revenue and stock price to gain investment, to the poor investment decisions such as bad infrastructure in India or the California power grid causing rolling blackouts Ultimately Enron collapsed under their own weight, call it greed, hubris, or incompetence and one cannot help but see similarities with ESG investing.

***

BlackRock, the largest investment firm in the world, has gone all-in on ESG investing. With over 9 trillion in assets it plans to make large – economy altering – decisions based on ESG investment strategies going into the future. In a letter, CEO Larry Fink described the important role ESG investing will have in BlackRock moving forward:

“Over the course of 2020, we have seen how purposeful companies, with better environmental, social, and governance (ESG) profiles, have outperformed their peers. During 2020, 81% of a globally-representative selection of sustainable indexes outperformed their parent benchmarks. This outperformance was even more pronounced during the first quarter downturn, another instance of sustainable funds’ resilience that we have seen in prior downturns…I am an optimist. I have seen how many companies are taking these challenges seriously – how they are embracing the demands of greater transparency, greater accountability to stakeholders, and better preparation for climate change…I have great confidence in the ability of businesses to help move us out of this crisis and build a more inclusive capitalism.”

Calm seas and sunny skies in the words of Larry Fink, failing to critique the outperforming metrics related to ESG come from their own research of sustainability markers by analytic firms using mark to market strategies to prop up investments. Not to mention their sustainability profile all based on speculative frameworks – without explicitly saying the need for more cash in hand will come from government printing leading to more inflation. Tariq Fancy – former CIO of sustainable investing for BlackRock – penned an op-ed citing that Wall Street is committing these ‘greenwashing’ tactics as a PR stunt rather than actually addressing social and environmental challenges. Furthermore, pulling the curtain back saying there is no definitive proof that investing in ESG funds will create a sizeable impact on any social and environmental challenges. It is undeniably clear that the ESG investing strategy is a bubble or a house of cards that is propped up on a faulty premise that can have dire economic, social, and environmental consequences and must be challenged by regulatory bodies for clarity and transparency. For reference, the global economy lost 2 trillion dollars in the financial collapse of 2008, and shareholders lost almost 74 billion from Enron. That means ESG failure with a proposed 40 trillion can be cataclysmic on a social, economic, political, and environmental level.

4 thoughts on “The Web That Binds Us: Origins, Explanation, and the Psychology of Doomed ESG Investing.”